Introduction

The National Statistical Office (NSO) has transitioned India’s Gross Domestic Product (GDP) base year from 2011–12 to 2022–23. This revision is a critical update intended to align economic statistics with current structural realities, new economic activities, and improved data sources.

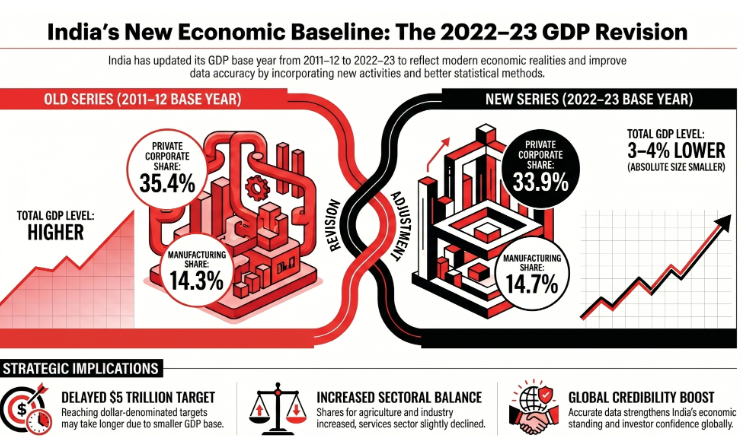

The most significant finding of the new series is a 3–4% reduction in the absolute size of India's GDP compared to estimates from the previous series. While this decline is unusual for a base-year revision, which typically captures unrecorded activity to increase the total, it appears to function as a correction for earlier overestimations. Despite the reduction in total size, annual growth trajectories remain broadly consistent with previous data, showing only minor variations of approximately one percentage point.

Key structural shifts identified include a higher share for agriculture and industry, a slight decline in the services sector’s dominance, and a significant reduction in the private corporate sector's contribution. These findings suggest that while India’s growth remains robust, achieving ambitious milestones such as a $5 trillion economy may take longer than previously projected.

Understanding GDP and the Revision Process

The Mechanics of GDP

Gross Domestic Product (GDP) represents the total value of all final goods and services produced within a country over a specific period. Compiled by the National Statistical Office (NSO), Indian GDP estimation adheres to international standards, specifically the United Nations System of National Accounts. To ensure accuracy, the calculation:

Excludes intermediate goods to prevent double counting.

Utilizes large datasets covering production, investment, consumption, and prices.

Encompasses national income, savings, and sectoral contributions.

The Purpose of Base Year Revisions

Base years serve as the benchmark for measuring price changes and economic growth. Revisions are typically conducted every 5–10 years to:

Capture New Activities: Incorporate industries and services that did not exist during the previous benchmark.

Refine Methodology: Implement improved statistical methods and data sources.

Reflect Structural Shifts: Acknowledge transitions, such as the movement of labor or capital between agriculture, industry, and services.

Enhance Credibility: Ensure statistics remain relevant for domestic policymakers and international investors.

Context and Background: The 2011–12 Series Controversy

The transition to the 2022–23 base year follows a decade of debate regarding the accuracy of the 2011–12 series (introduced in 2015). Analysts and economists raised several concerns:

Inconsistency with Indicators: Manufacturing growth figures often appeared stronger than what was reflected in other industrial data.

Corporate Sector Weighting: The private corporate sector’s contribution to GDP saw a sharp, questionable increase in the 2011–12 revision.

Data Reliability: Questions were raised regarding the specific data sources used for corporate measurement.

International Rating: The International Monetary Fund (IMF) previously assigned India a “C” rating for the quality of its national accounts data, signaling a need for systemic improvement.

Key Findings of the 2022–23 GDP Series

The new series introduces notable adjustments to the scale and composition of the Indian economy.

1. Adjustments to Economic Size and Growth

Total GDP Size: The absolute size of the economy is estimated to be 3–4% smaller than the previous series suggested. This is viewed by experts as a "correction" of the potential overestimations inherent in the 2011–12 series.

Growth Trajectory: Annual growth rates have not seen a radical shift. The difference between the old and new series is approximately one percentage point, indicating that the underlying pace of economic expansion remains stable.

2. Sectoral and Institutional Shifts

The revision has rebalanced the perceived contributions of various sectors to the national economy.

Metric | Findings under the 2022–23 Series |

Agriculture & Industry | Share of GDP has increased, likely due to better data sources and improved measurement. |

Services Sector | Remains the dominant sector, though its relative share has declined slightly. |

Manufacturing | Relative share increased from 14.3% to 14.7%; however, absolute output size fell by 1.5–1.6%. |

Private Corporate Sector | Contribution of the non-financial private corporate sector fell from 35.4% to 33.9%. |

Household & Informal Sector | Showed a slight increase in share, reflecting better measurement of informal and agricultural activities. |

Strategic and Economic Implications

Impact on National Targets

The reduction in the absolute size of the GDP has a direct impact on long-term goals. Specifically, the timeline for India to reach the $5 trillion economy milestone may be extended, as the starting point for that trajectory is now lower than previously recorded.

Enhanced Policy Accuracy

A more realistic assessment of the economy allows for:

Effective Planning: Policymakers can design interventions based on accurate sectoral data.

Prioritization: Changes in sectoral shares (such as the rise in agriculture and industry) may lead to shifts in government focus and resource allocation.

Global Credibility: Reliable data is essential for maintaining investor confidence, improving credit ratings, and facilitating international economic comparisons.

Transparency and Future Requirements

To maintain the integrity of these new estimates, economists emphasize the need for the government to provide:

Detailed explanations of the updated data sources.

Clear documentation of the statistical methodologies employed.

Ongoing transparency to prevent the recurrence of controversies that shadowed the 2011–12 series.

Conclusion

The revision of the GDP base year to 2022–23 is a significant step toward modernize India's economic reporting. While the series reveals a slightly smaller economy than previously thought, it offers a more nuanced and accurate picture of sectoral contributions and institutional roles. This precision is vital for the design of robust economic policies and for ensuring India’s continued integration and credibility within the global financial landscape.