Introduction

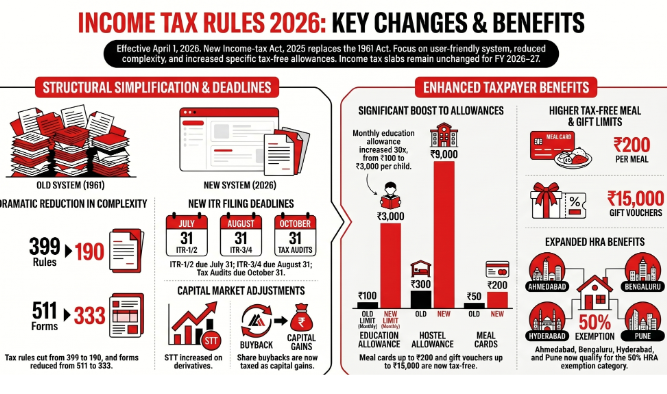

On March 20, 2026, the Finance Ministry notified the Income Tax Rules, 2026, which are set to take effect on April 1, 2026. These rules are designed to operationalize the Income-tax Act, 2025, which effectively replaces the long-standing Income-tax Act of 1961. The primary objective of this regulatory overhaul is structural simplification, significantly reducing the volume of rules and forms to create a more user-friendly tax environment.

Key highlights of the transition include a drastic reduction in the number of tax rules and forms, substantial increases in tax-free limits for employee allowances (such as education and hostel allowances), and specific adjustments to Securities Transaction Tax (STT) for derivatives. Despite these structural changes, income tax slabs for the 2026–27 fiscal year remain unchanged.

Regulatory Framework and Structural Simplification

The transition from the 1961 Act to the Income-tax Act, 2025, marks a major shift in India’s fiscal administration. The accompanying Income Tax Rules, 2026, emphasize efficiency through consolidation:

Rule Reduction: The total number of tax rules has been streamlined from 399 to 190.

Form Consolidation: The number of tax forms has been reduced from 511 to 333.

Implementation Timeline: Notification occurred on March 20, 2026, with full effectiveness scheduled for April 1, 2026.

Individual Taxation and Compliance

Tax Slabs and Deadlines

For the Financial Year 2026–27, there are no changes to existing income tax slabs. However, the rules clarify specific filing deadlines for various categories of taxpayers:

Category | Filing Deadline |

ITR-1 & ITR-2 | July 31 |

ITR-3 & ITR-4 (Non-audit) | August 31 |

Tax Audit Cases | October 31 |

House Rent Allowance (HRA)

The rules have expanded the 50% exemption category for HRA to include four additional major cities:

Ahmedabad

Bengaluru

Hyderabad

Pune

The updated rules also mandate increased transparency and stricter verification processes for HRA claims.

Revised Employee Benefits and Perquisites

The 2026 Rules introduce significant updates to the valuation and tax-free limits of various perquisites and allowances.

Daily and Annual Benefits

Meal Benefits: Under the old regime, the tax-free limit for meal cards has been increased from ₹50 to ₹200 per meal.

Gift Vouchers: Tax-free limits for gift vouchers are set at ₹15,000 per year.

Education and Transport Allowances

There have been substantial increases in the monthly tax-free limits for child-related allowances:

Children Education Allowance: Increased from ₹100 to ₹3,000 per month per child.

Hostel Allowance: Increased from ₹300 to ₹9,000 per month per child.

Transport Sector Allowance: The maximum limit has been increased to ₹25,000 per month.

Employer-Provided Perquisites

The taxation of company cars and concessional loans has been refined:

Company Cars: Monthly taxable value is ₹8,000 for engines ≤ 1.6L and ₹10,000 for engines > 1.6L.

Concessional Loans: Taxed based on the difference relative to the SBI lending rate. Loans ≤ ₹2 lakh or those taken for medical emergencies remain tax-free.

Capital Market and Corporate Changes

The new rules introduce higher costs for derivative trading and shift the tax burden of share buybacks to the investor.

Securities Transaction Tax (STT) Increases

Instrument | Previous Rate | New Rate |

Futures | 0.02% | 0.05% |

Options | 0.1% | 0.15% |

Share Buybacks

Under the new framework, share buybacks are now taxed as capital gains, altering the tax treatment for shareholders participating in corporate repurchases.

Institutional Oversight: CBDT

The Central Board of Direct Taxes (CBDT) remains the primary institution overseeing these changes.

Statutory Basis: Constituted under the Central Board of Revenue Act, 1963.

Leadership: Currently chaired by Ravi Agarwal.

Headquarters: New Delhi, India.

Related Policy Developments (March 2026)

The notification of the Income Tax Rules, 2026, occurred alongside several other significant legislative and diplomatic developments:

Chhattisgarh Freedom of Religion Bill, 2026: Proposed state legislation.

Promotion and Regulation of Online Gaming Act, 2025: A regulatory framework for the gaming sector.

International Cooperation: A Nuclear Energy Deal regarding Small Modular Reactors (SMRs) between the US and Japan, and a Memorandum of Understanding (MoU) between India and Bhutan regarding postal cooperation.