Introduction

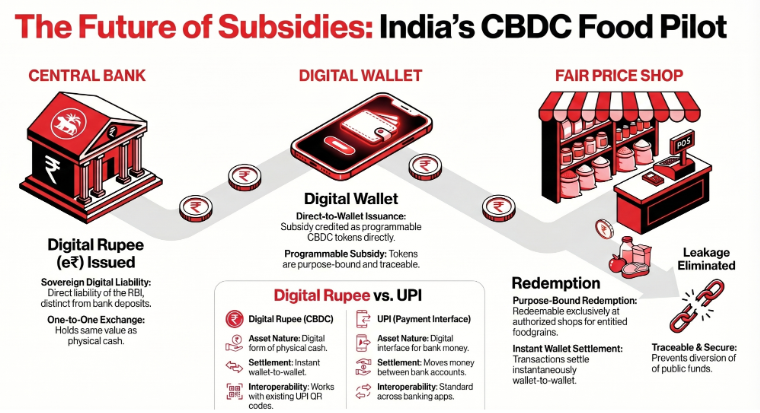

India has initiated a landmark reform in its Public Distribution System (PDS) by launching a Central Bank Digital Currency (CBDC) pilot for food subsidy distribution in Puducherry. Operating under the Pradhan Mantri Garib Kalyan Anna Yojana (PMGKAY), the project integrates the Digital Rupee (e₹) into the existing Direct Benefit Transfer (DBT) framework. The primary innovation of this pilot is the use of programmable, purpose-bound tokens that ensure subsidies are used exclusively for entitled foodgrains at authorized Fair Price Shops (FPS). By leveraging the sovereign nature of CBDC, the initiative aims to eliminate fund diversion, enhance transparency, and streamline the national food security ecosystem through instant, traceable, and secure digital transactions.

Analysis of the CBDC Pilot Initiative

The Puducherry Pilot Framework

The pilot program marks a strategic shift in how government subsidies are delivered and utilized. It is currently being executed through a multi-agency coordination effort involving the following stakeholders:

Government of Puducherry: Local administration for the initial rollout.

Reserve Bank of India (RBI): The issuing authority of the Digital Rupee.

Public Financial Management System (PFMS): The platform managing the transfer of funds.

Canara Bank: Partnering financial institution for implementation.

Following the initial phase in Puducherry, the government intends to expand the initiative to other Union Territories and broader beneficiary groups.

Key Technological Features: Programmability and Purpose-Binding

The defining characteristic of this CBDC application is its "programmable" nature, which distinguishes it from traditional cash or standard digital transfers.

Restricted Redemption: Subsidy tokens are credited directly to beneficiary wallets but are programmed to be redeemable exclusively at authorized Fair Price Shops (FPS).

Elimination of Leakage: Because the tokens are purpose-bound, they cannot be diverted for non-essential or unintended purchases, ensuring the integrity of the food security mandate.

Efficiency and Traceability: The digital cash mechanism allows for instant settlement and full traceability of funds from the central bank to the end merchant, reducing friction within the PDS.

Understanding India’s Central Bank Digital Currency (e₹)

Definition and Legal Status

The Digital Rupee (e₹) is the digital form of India’s fiat currency. It possesses several core attributes:

Sovereign Liability: Unlike digital money in commercial bank accounts, which is a liability of that bank, CBDC is issued directly by the RBI and represents a direct sovereign liability.

Legal Tender: It holds the same value as physical cash and is exchangeable one-to-one with paper currency.

No Interest: Because it mimics physical cash, no interest is paid on balances held in CBDC wallets.

Classification of CBDC

The RBI has established two distinct categories for the Digital Rupee to serve different sectors of the economy:

Feature | Retail CBDC (e₹-R) | Wholesale CBDC (e₹-W) |

Primary Users | General public and everyday businesses. | Financial institutions and intermediaries. |

Use Cases | Instant peer-to-peer (P2P) and peer-to-merchant (P2M) transactions. | Large-value transactions, secondary market trades in G-Secs, and inter-bank lending. |

Benefits | Provides a safe digital store of value for the public. | Reduces settlement costs and mitigates counterparty risks. |

CBDC vs. Unified Payments Interface (UPI)

While both systems facilitate digital payments, they operate on fundamentally different financial architectures:

Payment Interface vs. Currency: UPI is a payment interface that facilitates the movement of existing money between commercial bank accounts. In contrast, the Digital Rupee is the currency itself.

Settlement Mechanism: CBDC transactions settle instantaneously wallet-to-wallet. This process bypasses the need for a commercial bank’s backend ledger, whereas UPI relies on the inter-bank settlement process.

Interoperability: To ensure user convenience and rapid adoption, e₹ applications are designed to be fully interoperable with existing UPI QR codes.

Strategic Implications and Conclusion

The integration of CBDC into the PMGKAY subsidy distribution represents a sophisticated evolution of the Direct Benefit Transfer (DBT) mechanism. By transitioning from a simple transfer of value to a programmable digital asset, the government can achieve:

Enhanced Accountability: Total visibility into the lifecycle of a subsidy unit.

Security: A highly secure digital environment for vulnerable populations to receive aid.

Systemic Reform: A significant reduction in the leakages and inefficiencies historically associated with the Public Distribution System.

The success of the Puducherry pilot will likely serve as a blueprint for the future of targeted government interventions in India.