Introduction

On February 24, 2026, India and France signed an amending protocol to the 1992 Double Taxation Avoidance Convention (DTAC). This protocol introduces a series of significant updates designed to modernize the bilateral tax framework, provide greater certainty for taxpayers, and stimulate the cross-border flow of investment, technology, and personnel.

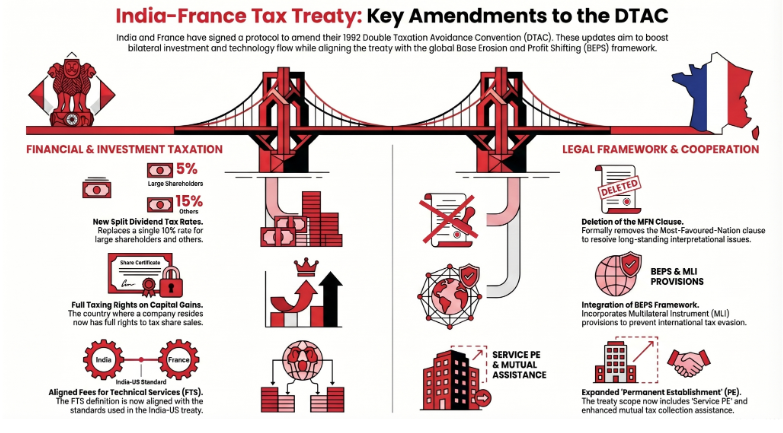

The amendments focus on critical areas of international taxation, including capital gains, dividend distribution, and the definition of technical services. Notably, the protocol formally eliminates the Most-Favoured-Nation (MFN) clause and integrates provisions from the multilateral Base Erosion and Profit Shifting (BEPS) framework. These changes align the bilateral agreement with current international standards and provide a more robust mechanism for tax cooperation and collection assistance between the two nations.

Detailed Examination of Key Amendments

The amending protocol introduces specific changes to the 1992 convention that clarify jurisdictional taxing rights and modify existing tax rates.

1. Capital Gains Taxation

The protocol establishes a definitive rule regarding the sale of company shares. Full taxing rights for capital gains arising from the sale of such shares are now granted to the jurisdiction where the company is a resident. This shift is intended to provide clear guidance on which nation has the authority to tax these specific assets.

2. Revised Taxation of Dividends

The previous single tax rate of 10% on dividends has been replaced by a split-rate system. This new structure differentiates between levels of capital ownership:

5% Tax Rate: Applicable to dividend recipients holding at least 10% of the company's capital.

15% Tax Rate: Applicable to all other cases of dividend distribution.

3. Procedural and Definitional Changes

MFN Clause Deletion: The protocol formally deletes the Most-Favoured-Nation (MFN) clause. This action is intended to resolve long-standing issues and uncertainties associated with its application.

Fees for Technical Services (FTS): The definition of FTS has been modified to align with the definition used in the India-US Double Taxation Avoidance Agreement, ensuring greater consistency across India's major tax treaties.

Permanent Establishment (PE) Scope: The protocol expands the definition of 'Permanent Establishment' by specifically adding 'Service PE,' which allows for the taxation of services rendered within a jurisdiction under certain conditions.

Strategic Alignment and International Standards

The protocol significantly updates the cooperative framework between the Indian and French tax authorities to meet modern international benchmarks.

Multilateral Framework Integration

The amendments incorporate the applicable provisions of the Base Erosion and Profit Shifting (BEPS) Multilateral Instrument (MLI). While India and France had already signed and ratified the MLI, this protocol explicitly embeds those provisions within the bilateral DTAC to ensure a seamless regulatory environment.

Enhanced Tax Cooperation

The agreement introduces modern standards for administrative cooperation:

Exchange of Information: Provisions have been updated to facilitate a more efficient flow of data between tax authorities.

Assistance in Collection of Taxes: A new article has been introduced to provide mutual assistance in the actual collection of tax liabilities, strengthening the enforcement capabilities of both jurisdictions.

Conclusion and Expected Impact

The amendments to the India-France DTAC represent a comprehensive update to a decades-old agreement. By aligning definitions with other major treaties (such as the India-US DTAA) and incorporating BEPS protections, the protocol aims to reduce litigation and tax uncertainty.

The anticipated outcomes of these changes include:

Increased Bilateral Investment: Clearer rules on capital gains and dividends are expected to encourage long-term capital flows.

Enhanced Regulatory Certainty: The removal of the MFN clause and the update of technical definitions provide a more predictable legal environment for multinational corporations.

Improved Enforcement: New mechanisms for the exchange of information and assistance in tax collection will aid both governments in addressing tax evasion and ensuring compliance.